68 minutes (with Q&A) ∙ 24 registrants

⮑ Ended WED SEP 18, 2024 5:08 PM CDT (Chicago)

✅ Full Q&A is included with this panelWhat Does 50 bps Mean? Our Panelists and Audience Discuss

If you missed the latest econvue panel, you can listen to our discussion in its entirety now. Part 2 of our Jackson Hole meeting at the end of August, our live panel took place immediately after the September 18th FOMC meeting. We were joined by members of the Chicago Financial Forum to discuss the historic Fed pivot, the first time rates were cut since March of 2020.

Our panelists include Chicago economists and econVue contributors Karim Pakravan, Michael Lewis, and Gordon Parrish. Other contributors to this not-to-be-missed debate: Michele Wucker, Richard Katz, Michael Boyd, Rich Manewal, Joel Ross, Mark Zoff, and Northwestern University professor of economics, Robert Gordon.

Most were surprised by the 50 bps move. Our public poll on X also got it wrong:

New Data: Was 50 bps Too Much?

Then on Oct 4th, the September employment report was released. Our panel thought that the Fed would cut another 50 bps by the end of this year, but after Friday’s robust jobs report, there is renewed speculation that the Federal Reserve could hold rates steady in November. Larry Summers was quick to say that Fed went too far last month. Given this new data, did Jay Powell act too quickly?

In his latest report, our panelist Michael Lewis reacted to the BLS report:

Stronger payroll gains, higher wages, lower unemployment. Today’s report ruffled Fed doves’ feathers on most every front. Barring a significant deceleration in inflation this month, the next step in the FOMC’s promised aggressive easing campaign should be a pause at the early November meeting. (But Powell & Co. have been following their hopes, not the data…)

The Lone Fed Dissenter

Our panelists noted the dissent of Federal Reserve board member Michelle Bowman, the first for an FOMC decision since 2005. It took several days for the blackout period to end, and for Governor Bowman to more fully explain her actions:

As the post-meeting statement noted, I dissented from the FOMC's decision, preferring instead to lower the target range for the federal funds rate by 1/4 percentage point to 5 to 5‑1/4 percent. Last Friday, once our FOMC participant communications blackout period concluded, the Board of Governors released my statement explaining the decision to depart from the majority of the voting members. I agreed with the Committee's assessment that, given the progress we have seen since the middle of 2023 on both lowering inflation and cooling the labor market, it was appropriate to reflect this progress by recalibrating the level of the federal funds rate and begin the process of moving toward a more neutral stance of policy. As my statement notes, I preferred a smaller initial cut in the policy rate while the U.S. economy remains strong and inflation remains a concern, despite recent progress.

Recent Views on Monetary Policy and the Economic Outlook: Governor Michelle W. Bowman, September 30, 2024, Board of Governors of the Federal Reserve System

My takeaways

The panel focused on the lead up to the 50 basis points cut, questioning both its rationale and potential impact on markets and the economy.

The panel questioned the sudden shift between 25 and 50 bps in the weekend leading up to the decision, perhaps signaling a change in forward guidance.

As economist Robert Gordon mentioned during our discussion, the exact amount of the first cut doesn’t really matter – what does is the amount of easing by year-end. He contributed much to our discussion of labor markets, housing, inflation and of course, productivity.

Michele Wucker’s concern that the impact of the rate cut on the real economy might not be as strong as the impact on markets is on point as US equity markets reach record highs after the Fed decision

Housing should benefit from lower interest rates, but while an acute shortage of housing exists, the pricing issue appears to be supply more than demand.

Labor is a lagging factor. We now know that even without the recent cut, that the labor market was quite strong in September.

It is not just about monetary policy. The group discussed the government's ability to finance budget deficits and debt, with suggestions from Michael Boyd as to how the Treasury could impact bond yields (a new Operation Twist?) and support the housing market.

He also raised the critical question: How do we measure growth and received an answer from Robert Gordon that is worth listening to more than once. ⧈ (44.51)

Rate cuts will impact variable consumer debt. But policies will matter more.

As Joel Ross said during our discussion, geopolitics matters. A conflict in the Middle East, which has certainly escalated since our discussion, could increase oil prices and therefore inflation.

As Richard Katz predicted, the Bank of Japan (BoJ) had initially planned to cut interest rates by 25 basis points in September, but did not. Now the consensus is that they will wait until December.

econVue subscribers will gain deep insights from our panelists, who are veteran Fed watchers. Thank you to our panel and our audience, who contributed so much to the off-the-record discussion. Your comments as always are deeply appreciated.

–𝓁𝓎𝓇𝒾𝒸

Editor-in-Chief & Moderator

econVue Panels are primarily a feature of paid membership. Explore your options! If you would like to participate in our next discussion, please sign up today.

👥 Panelists

Michael Lewis

Michael Lewis is the founder of FMI. Before founding FMI, Mr. Lewis was an economist at Data Resources, Inc. and Atlantic Richfield Co. He was Chief Economist from 1978 to 1982 at Stein Roe & Farnham. He is kno…

📍Chicago

Karim Pakravan

Karim Pakravan is an academic, global finance specialist and consultant in the fields emerging markets, international finance, monetary policy and banking regulation.

📍Chicago

◻ Discussed on this Panel

Topics

Federal Reserve rate cuts and economic uncertainty

Bank of Japan's plans

Inflation rates, rate cuts, and election impact

The US central bank's dual mandate and interest rate cuts

Mortgage rates, home sales, and inflation discussion

Inflation drivers and labor market dynamics

Productivity, GDP, and GDI

Government financing, fiscal policy, and the yield curve

⧉ Insights

What are the international implications of a 50 bps cut by the Fed?

“What I think is going to happen is it’s going to accelerate the easing of monetary policy in all the major countries, with the exception of Japan. I think there will be a boost to confidence and potentially economic growth in 2025, which is helpful for everybody. Also lower interest rates, as I said in the previous panel discussion we had, is going to help emerging markets in terms of their debt servicing costs. So it looks fairly positive for them as as a whole. Inflation is still a problem in many emerging markets so the easing there is going to be at a little bit of a slower pace. ⧈

Basically, where we'll be at the end of the year is going to matter. And it doesn't matter if it's 50 right now. And so I go back to my point saying I think Powell basically wanted 1% by the end of the year, and then he just decided to do 50 right now, not because he just felt like it, but maybe he was worried that if he didn't do that, it would disrupt the markets again. ⧈

Key moment ⤵

Were you surprised by the 50 bps cut?

“We were thinking a few months ago that they wouldn’t cut at all at the end of this year and that we would stick around the current five and a half at that time. And we’re not surprised given the commentary by Powell and others that they went ahead and eased today. But we are surprised that the eased 50 bps. ⧈

My colleague Gordon Parrish was pointing out to me this afternoon that in March ‘22, the expectation for the funds rate was 2.8: ‘The striking parallel is that in March 2022, when the Fed increased rates for the first time to confront inflation their dot plot said our terminal rate is going to be 2.8% in 2024. And then we'll be done. Of course, that's not what happened. They went all the way up to 5.5%. They stayed there for 15 months. And inflation is still clearly above target. Today, they issue a new dot plot, a very aggressive plan to cut rates over the next two years. And they're ending up at 2.9%, which is the same place. And after being so spectacularly wrong back in 2022, the question is why are they doing any better now?’ ⧈

Key moment ⤵

⧉ Backgrounder

OCT 6, 2024

Recommended Reading

Transcript of Press Conference, Chair Jerome Powell, Sep 19, 2024 Federal Reserve

Statement by Michelle Bowman, Sep 20, 2024, Federal Reserve

econVue featured article:

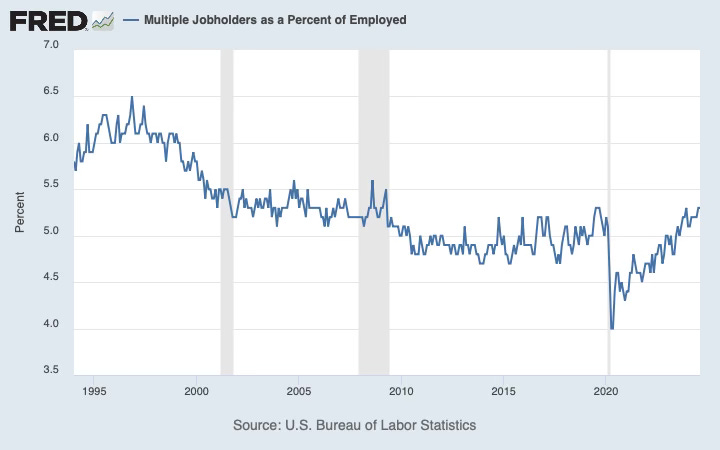

Regarding employment and multiple job holders: