Silver Shock

The Silver Standard: China and America's Critical Minerals Strategy

A Critical Announcement

On November 7th last year, the US Department of the Interior quietly released its final 2025 Critical Minerals List.1 For the first time, silver was formally designated as a critical mineral. No longer just an investable precious metal, silver underpins the electronics industry, solar manufacturing, and key infrastructure and defense systems. Its industrial superpower: it is the most conductive metal for electricity on earth. This new designation signals a shift in Washington’s thinking about critical resources.

❝ From a policy perspective, China’s dependence on silver could serve as a strategic fulcrum to offset American vulnerability in rare earths and other critical resources. This crisis may provide the political and market impetus necessary to act.

Price Volatility & China

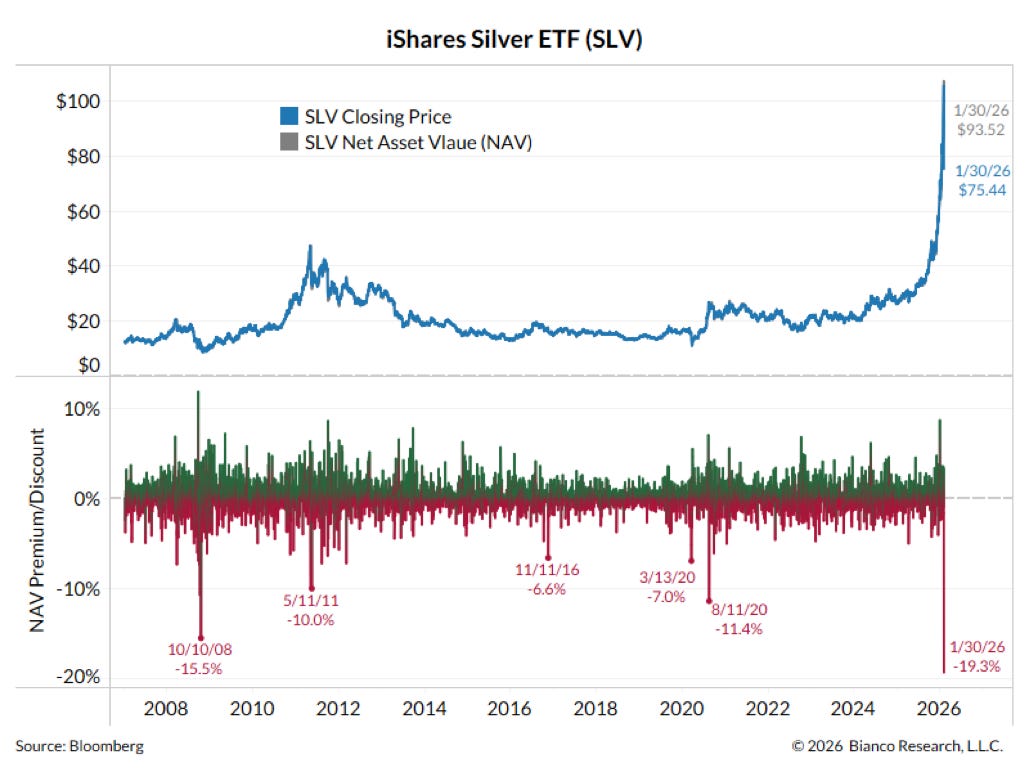

Since early November, the silver price has surged, from $48.15 on Nov 7 to a recent high of $121.79 before retracing sharply on Friday to $85.25. Even after this pullback, prices remain dramatically elevated relative to early autumn.

In the investment world, all eyes are on futures markets and China. Gold’s increase in value is largely seen as a function of central bank purchases over time, particularly the People’s Bank of China. Silver, however, is not widely held by central banks. Its dual use, as a store of value and an industrial commodity, has given it both a retail and commercial base of investors.

What is different this time is that there is a wide divergence between silver prices in Western financial markets and physical markets in Shanghai, where silver is selling at a significant premium of around 40%. This premium suggests tight physical supply and strong local demand, though it has also prompted questions about market structure and policy intervention. (A new website tracks these differentials in real time: metalcharts.org/shanghai.)

The discount to NAV (net asset value) is also enormous in US markets, reaching 19.3% as of Jan 30, closer to the crypto ETF discounts such as GBTC to Bitcoin than to precious metals. What this uptick means is that SLV ( the iShares Silver Trust) is trading almost 20% below the value of the physical silver it holds; historically this discount has been only 1-2%. In the absence of a remarkable decline in industrial demand, this kind of movement signals liquidity stress. Traders are describing this as a “six-sigma shock” or a statistical outlier. Especially since silver, unlike gold, is not a balance sheet stabilizer; it has a dual use as a speculative asset and an industrial commodity.

The simultaneous fall in the prices of other assets such as gold and bitcoin supports the liquidity thesis. During a liquidity crunch, investors sell what they can. There is speculation that massive shorts that went wrong broke the silver market, and there could be collateral damage at institutions that followed this path. At risk is the concept of precious metals as a safe haven asset, given recent volatility.

Here in Chicago, the CME Group raised COMEX margin requirements on these trades.

What happened last Friday? As Jim Bianco notes on X:

❝ Yesterday’s 19% discount to NAV broke the record set on 10/10/2008, the day the TARP was introduced during the Global Financial Crisis…It doesn’t mean we will automatically see a firm fail, but the silver market needs to correct itself quickly; otherwise, it probably will.

Market Reaction

In addition to speculation about Chinese industrial weakness, widespread liquidity issues, there are two confounding factors. The first was the announcement on Friday morning that Kevin Warsh would be President Trump’s nominee for the Federal Reserve Chair. He is neither a classic hawk nor dove, and is known to favor shrinking the Fed’s balance sheet, which means less quantitative easing and tighter financial conditions. The threat of war in the Middle East is also looming closer, as US military assets move closer to striking distance of Iran.

Friday’s shock may ultimately prove financial rather than structural. But volatility does not erase vulnerability. Silver now sits at the intersection of electrification, liquidity, and geopolitics — a small metal carrying outsized weight in modern industry.

The United States has labeled silver as a critical mineral, and markets are attempting to set its value. When silver moves, there could be multiple causes, and so in a volatile geopolitical environment, price variations should be expected. Still, the level of change is surprising. What remains uncertain is whether this episode reflects transient liquidity pressure or is an early signal of deeper structural change, especially in China. Noted with concern at the beginning of a potentially tempestuous week: Chinese EV maker BYD suffered a 30% fall in sales in January, as government subsidies came to an end.

Silver is Everywhere

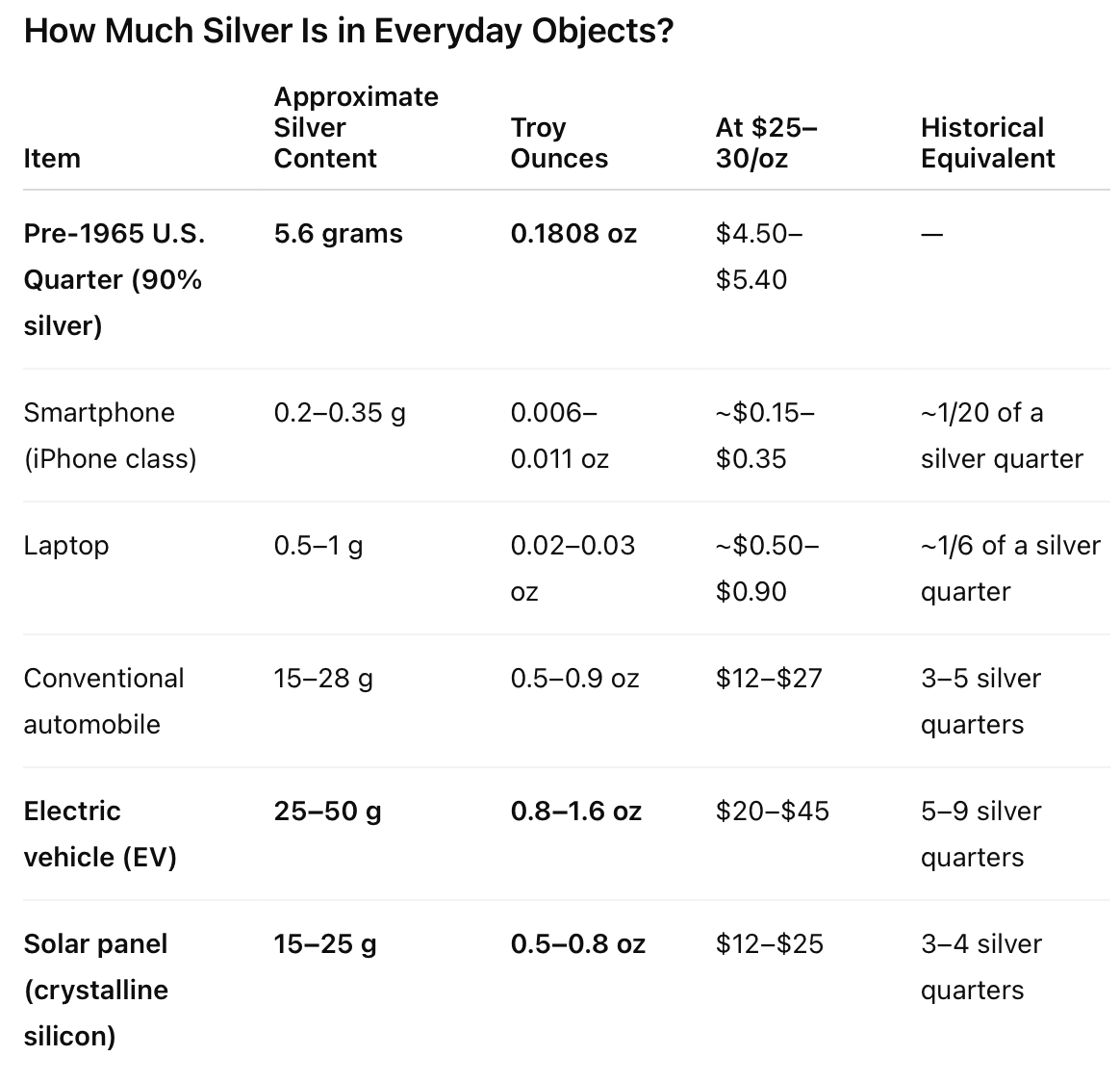

Beyond the price action, however, is a growing realization of the importance of silver in 21st century life. Previously, silver’s principal use was as money. If you have an old silver quarter, it is now worth many times its face value. You still have silver in your pocket; it is now powers your mobile phone, sits within your laptop, and runs power through your car’s electrical systems.

The strength in the price of silver has coincided with increased usage in Chinese manufacturing. It is not merely a speculative phenomenon, but reflects sustained structural growth in industrial demand. While attention has focused on China’s dominance of rare earths, China remains dependent on imported silver to power its critical export machine. Yet this is not the first time China’s economic system has been closely tied to silver. Over the past century, silver’s role in China has been transformed: it once served as the foundation of the country’s monetary standard.

Silver and China in the 20th Century

In the early 20th century, China was one of the few remaining countries whose monetary system was tied to silver. The rest of the world was on gold. After falling for several years, the global price of silver began to rise sharply in 1931, triggered by Britain’s decision to depreciate the pound against gold, followed by the US doing the same in 1933 with the dollar. A year later, the United States passed the Silver Purchase Act2 a measure driven largely by domestic political pressures that aimed to raise further silver prices.

Milton Friedman and Anna Schwartz interpreted this episode of rising silver prices as a reversal of China’s earlier insulation from global deflation.3 Weak silver prices initially functioned much like a depreciated currency, supporting exports. They believed, as was the official view at the time, that the subsequent appreciation of silver and silver outflows led directly to a contraction in the money supply and deflation, putting huge strains on the Chinese economy.

Later research by economists Loren Brandt and Thomas Sargent, based on evidence that was not available to Friedman and Schwartz, challenged the role of US silver purchases in China’s economic difficulties in that era.4 They offered a more nuanced interpretation:

❝ Recently compiled evidence about events in China are described and interpreted in light of a model of free banking under a commodity standard. Our interpretation is that the U.S. silver purchase program did not set off a chain of bad economic events which eventually forced China off of silver and onto a fiat standard. Rather, China was forced off silver by its own government, which wanted to make itself the beneficiary of the capital gain associated with the appreciation of silver and to relieve itself of the restrictions that are imposed on government finance by a commodity standard.

Brandt and Sargent document that the money supply did not collapse. The decline in silver was more than offset by increases in banknotes that were convertible on demand into silver. The promise of convertibility was maintained over the entire episode. In their interpretation, China’s departure from the silver standard was a political decision by the Kuomintang government, not a collapse imposed from abroad. It gave the KMT greater fiscal flexibility and room to run deficits, and allowed it to capture a significant portion of the appreciation in silver through a nationalization program highly favorable to itself.

This fascinating episode in monetary history remains debated among economic historians, but it illustrates a broader principle: when a nation’s monetary or industrial system is closely tied to a globally traded metal beyond its policy control, there can be domestic consequences. However, causation is not so easily determined without hard evidence.

Silver is no longer China’s monetary standard, but it now critical to its industrial power base in solar energy, automobiles, and electronics. Dependence on silver is a vulnerability in ways that could not have been imagined almost a century ago.