Tariffs Are Not About Prices

And consumer confidence is not consumption

As a tidal wave of tariffs rolls in around the world, weak consumer confidence numbers have sparked fears of a coming recession, driven by fears of falling consumption. At least in the US however, this is not historically true. Americans are born and bred to consume, and paradoxically, anxiety only seems to increase their propensity to spend. The interplay between financial conditions and consumer behavior is complex.

This is a feature of a psychological phenomenon called catastrophic thinking.1 In February of 2025, a survey by Creditcards.com2 found the following:

Doom Spending ⧉

-1 in 5 Americans are buying more than usual, most driven by Trump’s tariffs

-3 in 10 Americans are purchasing items in preparation for another pandemic

-42% of Americans are or will start stockpiling items, mainly food and toilet paper

-1 in 4 Americans have made large purchases since November in fear of Trump’s tariffs

-1 in 5 Americans say they are “doom spending” — purchasing items excessively or impulsively in response to fears or anxiety about future events

-23% of Americans expect to worsen or go into credit card debt this yearFor example, after 9/11, confidence fell by 25%, but spending only fell by 1.3% and rebounded within a month. This pattern repeated during Covid, when direct fiscal stimulus added fuel to the fire, driving retail spending to all-time highs. While culturally, Chinese consumers react to stress by saving more, US consumers spend more in times of uncertainty as a form of emotional reassurance, a pattern reflected in post-crisis retail surges.

A Short History of US Confidence/Consumption Dips

Oct 1987 Crash: Confidence dropped, but consumption barely moved.

9/11 Attacks: A sharp confidence drop, but spending rebounded quickly.

Great Financial Crisis: Massive declines in both.

COVID-19: Unprecedented hit to both, but consumption rebounded faster than expected, once restrictions ended and businesses reopened, utilizing a $2.6T jump in household savings in 2020.

2025 Tariff Shock (Liberation Day): So far, a modest confidence and consumption dip—pending further developments.

Why was the Great Financial Crisis different? The entire banking system was at risk. The wealth effect was real: the stock market and real estate values plummeted. Access to credit tightened dramatically, and unlike during Covid, there was no immediate stimulus.

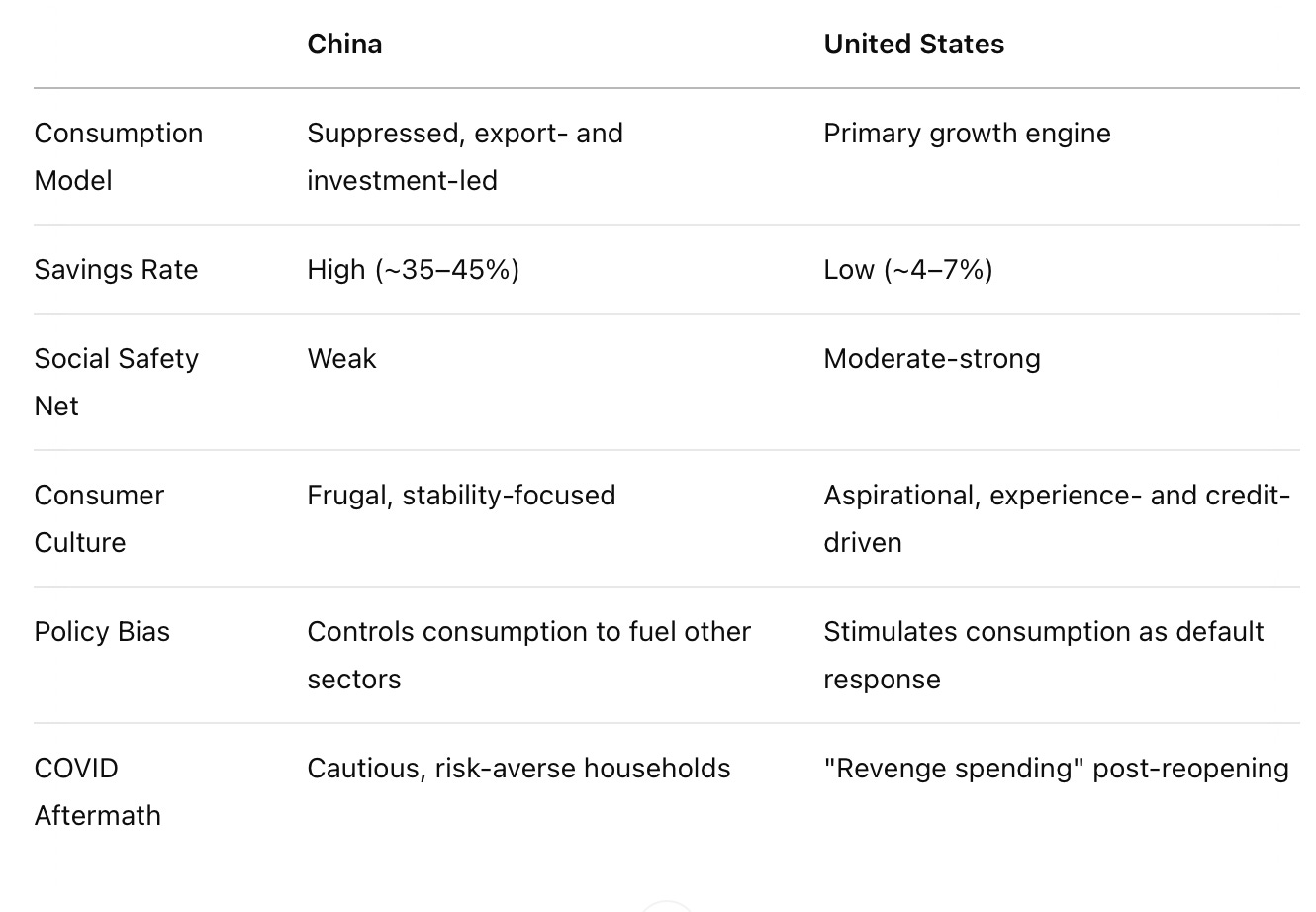

China might take a lesson here, in terms of how long the GFC recovery took in the US absent fiscal stimulus, and its own tepid post-Covid consumption after its people endured two years of lockdowns. Chinese consumers remained cautious long after lockdowns ended. This was not due to sentiment or lack of savings, but because of cultural and structural issues: a weak social safety net, overtaxation of consumption, lingering policy uncertainty, and the negative wealth effect based on property prices and equity markets.

The Big Picture: China vs the US